Wage Garnishment After Debt Lawsuit

By Sued For Debt Help Editorial Team | Reviewed for legal context by David McNickel

Wage garnishment is one of the most direct enforcement tools available to a judgment creditor after winning a debt lawsuit. It allows the creditor to collect money directly from a debtor’s paycheck – automatically, without the debtor’s cooperation.

Understanding how the process works, what limits apply, how employers are involved, and what options exist to stop or reduce garnishment is essential for anyone facing this situation.

Review other collection risks after a debt judgment.

How Wage Garnishment Works

Wage garnishment in the context of a civil debt lawsuit follows a specific procedural path. It cannot begin until a court has entered a money judgment. Once a judgment exists, the process moves quickly:

- The judgment creditor files an application for a writ of garnishment (sometimes called a writ of execution) with the court that issued the judgment.

- The court issues the writ, which is served on the defendant’s employer. The employer is legally required to comply.

- The employer begins withholding the applicable percentage from each paycheck and remits those funds to the court or directly to the creditor, depending on state procedure.

- The debtor receives notification – in most states, the employer is required to notify the employee when a garnishment begins, and the court or creditor may also send notice.

- Garnishment continues until the full judgment amount (plus post-judgment interest) is satisfied, or until a court order stops it.

The entire process from judgment to active garnishment can happen within weeks, and in some states within days. The debtor may learn of the garnishment only when they see a reduced paycheck.

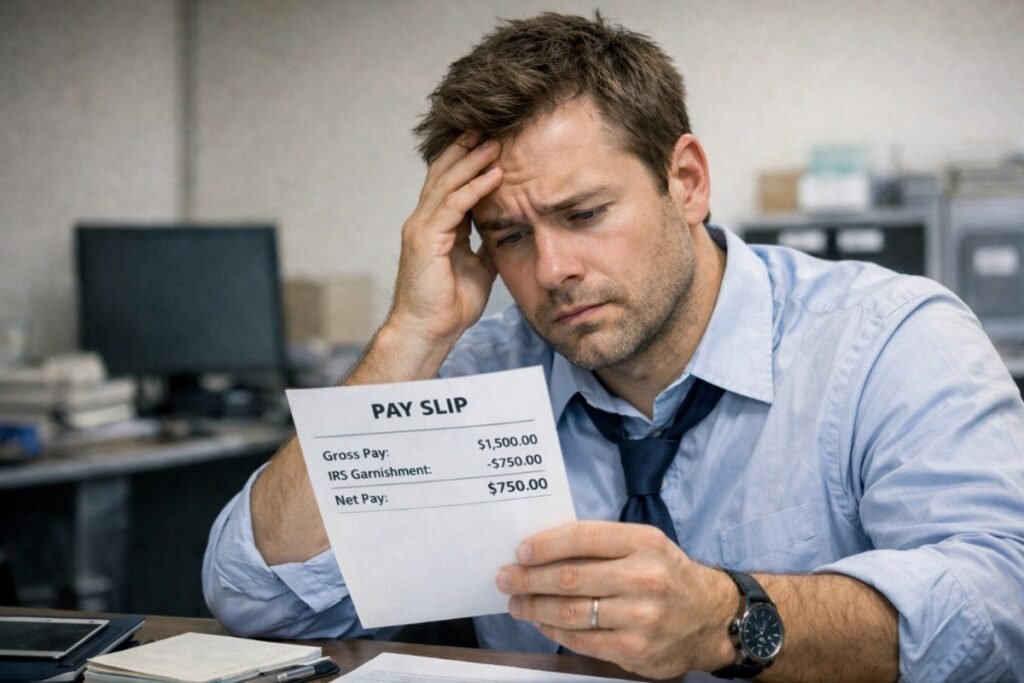

Federal Limits on Wage Garnishment

Federal law establishes minimum protections for debtors subject to wage garnishment. The Consumer Credit Protection Act (CCPA) limits the amount that can be garnished from disposable earnings (earnings remaining after legally required deductions like taxes and Social Security).

Under the CCPA, the maximum amount that can be garnished per pay period is the lesser of:

- 25 percent of the debtor’s disposable earnings, OR

- The amount by which disposable earnings exceed 30 times the federal minimum wage per week (currently $7.25/hour, so 30 x $7.25 = $217.50 per week)

For most full-time workers earning above minimum wage, the 25 percent cap is the binding limit. For lower-income workers, the 30 times minimum wage formula often results in a smaller garnishable amount.

The CCPA also prohibits employers from firing an employee solely because of a single wage garnishment. However, this protection does not extend to employees facing multiple simultaneous garnishments.

Different types of debts have different garnishment limits under federal law. Child support and alimony can result in higher garnishment percentages. Student loan garnishment by the federal government operates under separate rules. State tax garnishments follow their own procedures. Consumer debt garnishments (credit cards, medical bills) are subject to the CCPA caps described above.

State Garnishment Rules

States can set stricter (more protective) garnishment limits than the federal floor, but not more permissive ones. Several states have adopted rules that are more favorable to debtors:

- Texas: Wage garnishment for consumer debt judgments is generally not permitted, with limited exceptions

- Pennsylvania: Wage garnishment for most consumer debts is prohibited; exceptions include support orders and some state debts

- North Carolina: Wage garnishment for consumer debts is generally not permitted

- South Carolina: Wage garnishment by most private creditors is prohibited

- California: Limits garnishment to the lesser of 25 percent of disposable earnings or the amount exceeding 40 times the state minimum wage

- Florida: Provides a head of household exemption that may protect up to 100 percent of wages for qualifying debtors

These state rules can significantly affect what a judgment creditor can actually reach. Understanding your state’s specific rules is essential for assessing your situation.

Employer Involvement

The debtor’s employer plays a central role in wage garnishment. Once served with a writ of garnishment, the employer is required by law to:

- Begin withholding the legally mandated percentage from the employee’s wages

- Remit withheld funds to the court or creditor as directed by the writ

- File any required responses or reports with the court confirming compliance

- Continue withholding until notified that the garnishment has been satisfied or released

Employers are prohibited from terminating an employee solely because of a single garnishment under federal law. Employers who fail to comply with a valid garnishment writ can be held in contempt of court.

The employer’s payroll department handles the withholding mechanically – it is not a discretionary decision. Once the writ arrives, the employer has no legal authority to refuse compliance.

Exempt Income That Cannot Be Garnished

Certain types of income are protected from garnishment under federal and state law, regardless of any court judgment:

- Social Security retirement, disability (SSDI), and SSI benefits

- Supplemental Security Income (SSI)

- Veterans’ benefits

- Federal employee retirement income

- Railroad Retirement benefits

- Black Lung benefits

- Unemployment insurance benefits (in most states)

- Workers’ compensation benefits (in most states)

Note that while these income types are exempt from garnishment, once they are deposited into a bank account and commingled with non-exempt funds, protecting them through a bank levy may require filing a claim of exemption.

Ways to Stop or Reduce Garnishment

Claim of Exemption

If you believe that some or all of your income is exempt from garnishment under state or federal law (including the head of household exemption in some states), file a claim of exemption with the court. The form and procedure vary by state. Once filed, the court schedules a hearing to determine whether the exemption applies.

Negotiate a Settlement or Payment Plan

Contacting the judgment creditor directly to negotiate a lump-sum settlement or payment plan can sometimes result in an agreement to suspend garnishment. Creditors often prefer a negotiated resolution over the administrative burden of ongoing garnishment, particularly if you can offer a meaningful lump sum. Any agreement to suspend or release the garnishment should be in writing.

Motion to Vacate the Judgment

If the underlying default judgment was improperly obtained – due to defective service or other grounds – filing a motion to vacate the judgment can halt garnishment pending the court’s decision. Courts may issue a stay of garnishment while the motion is pending.

Bankruptcy Filing

Filing a bankruptcy petition triggers an automatic stay under 11 U.S.C. § 362 that immediately stops wage garnishment, bank levies, and all other collection activity. The stay goes into effect the moment the bankruptcy petition is filed. Whether the underlying debt can be discharged depends on the chapter filed and the nature of the debt.

Return to Hub: Explore additional articles explaining common consequences of debt judgments.

The information on this website is for general informational purposes only and should not be considered legal advice. Suedfordebthelp.com is not affiliated with any credit agency, law firm, or government agency.